Are You Looking For An Experienced Mortgage Professional In Vancouver?

My goal is to make your home ownership dreams come true.

ANNA SMITH

Happy Client

" Deb is fantastic to work with and refer to clients because she is fast, efficient and reliable. It is a pleasure to spread the good word of her enthusiastic work, helping clients with their new home purchases. Deb is not one to give up easily; she will work long and hard for her clients to get a solid outcome for them. "

Finding the best mortgage can be frustrating. It doesn't have to be when you follow my 3 step plan.

STEP ONE

Connect with me!

The process starts when you get in touch. Let's take a look at your financial situation and put together a plan for your first/next mortgage!

STEP TWO

Discuss your options.

When it comes to mortgage financing, you have options! Let's clarify those options, so you can make the best decision for your needs.

STEP THREE

The Paperwork.

Paperwork is the nitty gritty of mortgage financing. I'll make sure you know exactly what is required of you at every step, limiting any delays.

STEP FOUR

Lifetime support.

Once I've arranged your mortgage, I'm not going anywhere! As long as you need a mortgage, you can trust that I'll be there to give you a hand.

Curious about what you might be able to afford?

Find out how much you can afford in 30 seconds.

Deborah Burnstein Mortgage Specialist

A Better Way - Mortgage Architects

C

604.202.7493

Email deb@debsmortgages.ca

Deb Burnstein

Deb is proud to be an original Vancouverite. She has come to the mortgage financing business via a very successful career in corporates sales including financing products. Her dedication to customer satisfaction and long-term relationships has paved the way to her success. Whether she is working with a first-time home buyer or helping seniors enhance their retirement income deb has the patience and compassion to guide all to a successful outcome.

Along with her passion for making her clients happy she enjoys outdoor activities like golfing, snowshoeing, and kayaking but can also be found travelling or at a music concert with family and friends. When not outside she is usually taking care of her insides with yoga and chocolate (not necessarily in that order).

Nice things people have said about working with me.

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.

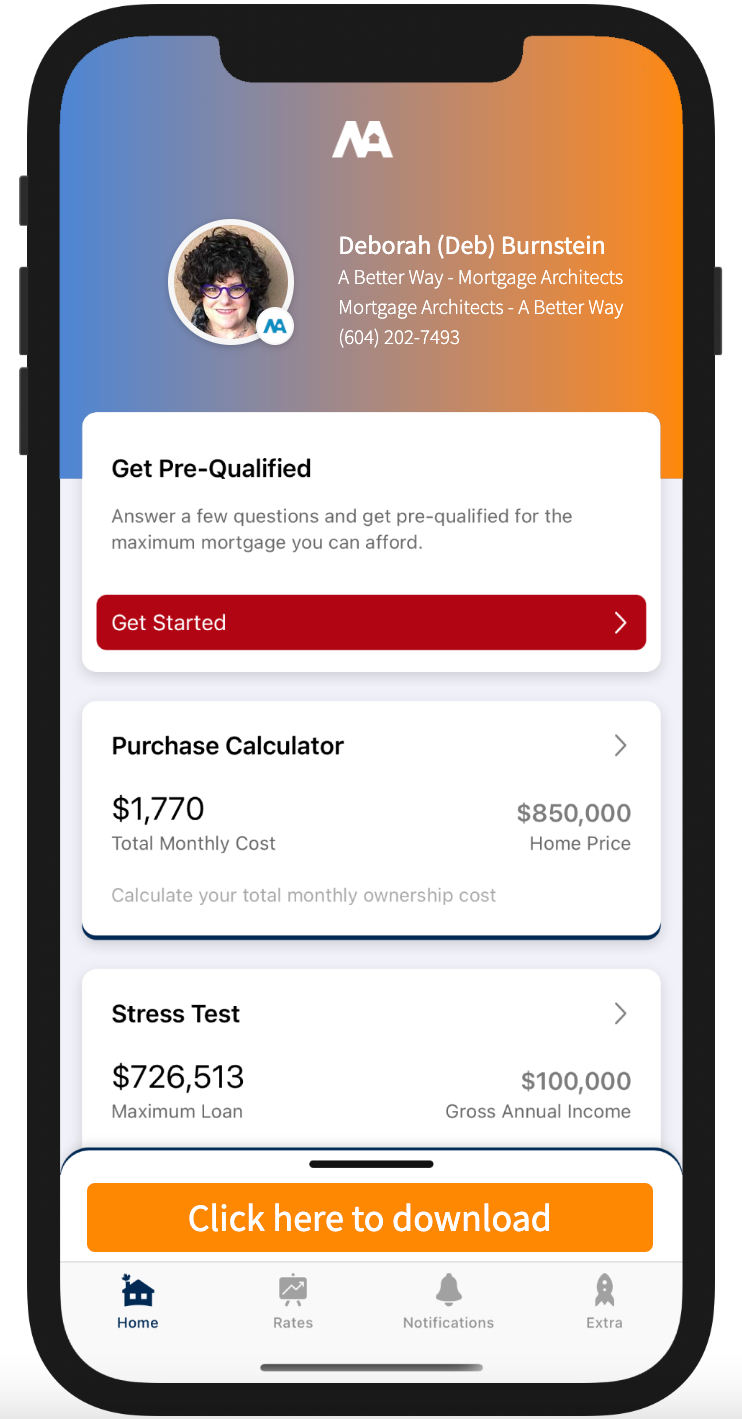

Download my Mortgage Toolbox App

Contact me

Contact Us

Get in touch

I'm committed to helping you in any way I can. Leave me a note and I'll get in touch with you shortly.

Everything you need,

all in one place

As a trusted mortgage provider, let me help you with these services.

Click through any of the services to learn more